Back in February, Dell, the world’s largest server maker, told Wall Street that it was planning on selling and delivering $15 billion in AI servers in its fiscal 2026, when will end in early November. Sales were a little more tepid than we and many on Wall Street had expected in the first quarter, which ended in May. Which is not good. But Dell booked $12.1 billion in new AI system orders during the May quarter and is sitting on a backlog of $14.4 billion in AI systems orders in total as the quarter ended, and it actually delivered $1.8 billion in AI systems in Q1 F2026.

So hitting that $15 billion target for the entire year looks like it is pretty much in the bag – so long as allocations of GPUs to Dell and its big customers (like Elon Musk’s xAI Grok model builder, which sourced half of the first phase of its 100,000 GPU-strong “Colossus” AI supercomputer from Dell) are sufficient to drive that revenue.

But, once again, we are worried about the margins that Dell and its OEM and ODM peers can derive from these massive AI supercomputers.

(And while we are thinking about it: They are not AI factories, but they are token factories. . . . and no matter what you call them, they are supercomputers. If you want to call something an AI factory, it is the whole datacenter. Maybe, given the cost and scale, ubercomputers or superdupercomputers. Google calls them hypercomputers, and that has a nice ring to it.)

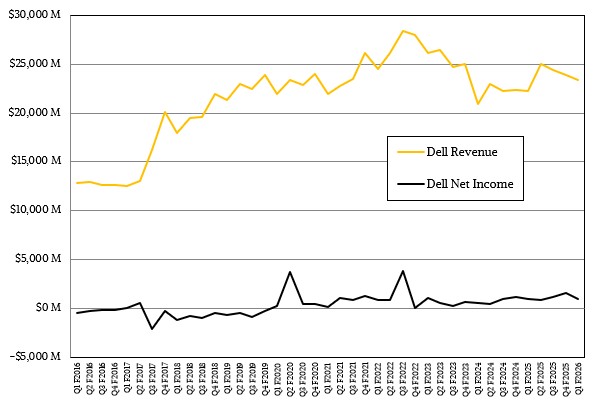

In any event, in the May quarter, Dell had $19.6 billion in product sales, up 9.1 percent, while services sales were $5.78 billion, down 5.5 percent.

We don’t care much about Dell’s PC business, except as a customer (we do Dell workstations and HPE laptops around this joint) and except for the fact that Dell drives revenues here that help its partnerships with parts suppliers, many of whom have server products and therefore gives Dell some leverage. (Think Intel and AMD, Nvidia, and the memory and flash makers.) This time around, Dell’s Client Solutions Group had $12.51 billion in sales, up 4.5 percent, but operating income fell by 10.8 percent to $653 million.

The good news is that the market for general purpose servers was better than many had expected, and it made up for a shortfall in PC profits and counterbalanced what we presume are pretty thin margins for AI supercomputers.

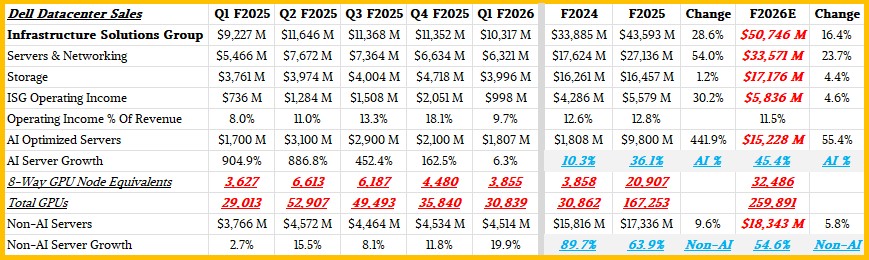

Dell’s Infrastructure Solutions Group had sales of $10.32 billion, up 11.8 percent. Within ISC, the Servers & Networking division had sales of $6.32 billion, up 15.6 percent. The Storage division had brought in $6.32 billion, up 15.6 percent. Take out the costs of all of this ISG business, and Dell had $998 million in operating income, which was up 35.6 percent and represented 9.7 percent of revenues. That may sound good, but the Q1 from the year-ago period was weak on the profits, so it is an easy compare.

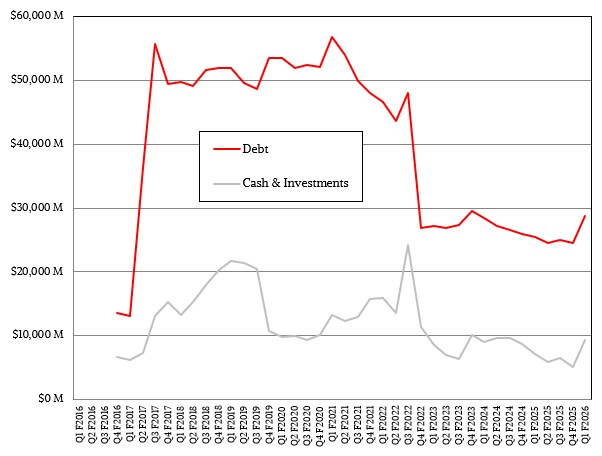

Add it all up and pay the taxes and other charges, and that $5.78 billion in net income helped Dell grow its cash hoard by 30.4 percent to $9.29 billion. However, Dell’s debt also increased by $4.21 billion from the end of fiscal 2025.

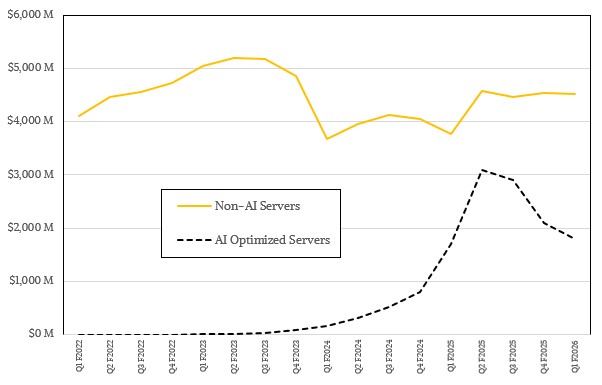

We have a model that stretches back to Q1 2024 that separates out AI server sales from non-AI server sales, which is synonymous with saying GPU-accelerated machines from CPU-only machines. Here are the trends for Dell:

We think Dell did about $1.81 billion in AI server sales in Q1 F2026, which by the way was about the same amount of money it brought in for all of F2024 in AI servers. So the ramp has been good. But as you can see, in absolute numbers, AI server revenues peaked for Dell two quarters ago when “Hopper” GPU systems were still going strong and “Blackwell” GPU systems were also ramping. This year, everyone is waiting for their Blackwell allocations from Nvidia, and more than a few customers decided to wait until they could get Blackwell B300 GPUs, which have 50 percent more oomph and 50 percent more HBM memory than the prior B200 GPUs.

As GPU system sales started to slide, CPU-only system sales to enterprises, governments, and other institutions picked up the slack and until this quarter filled in the gap.

In the next quarter, Dell says it will ship $7 billion worth of AI systems for revenue as traditional server sales soften against their usual sales rate, which tells us that maybe Dell offered a lot of deals to move traditional iron this quarter so it could fill in the AI pothole. But with $7 billion in sales next quarter, AI system revenues will be its biggest category by far and will outsell traditional servers by a factor of 7 to 4.

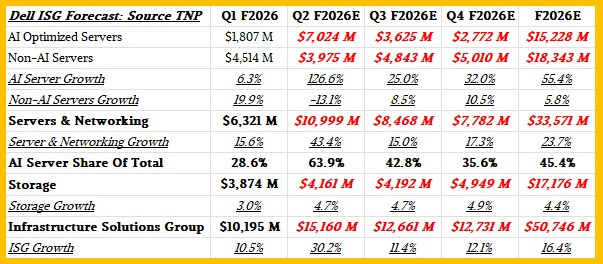

Given what Dell’s top brass said on the call with Wall Street analysts, here is our F2026 forecast for Dell’s ISG:

AI system growth will skyrocket by 2.3X in Q2 F2026 to $7.02 billion, we reckon, and traditional, non-AI server sales will fall by 13.1 percent to just under $4 billion. The Server & Networking division will grow by 43.4 percent to around $11 billion, setting a new high that we do not think Dell will repeat this year. If the Storage division grows modestly – call it around 5 percent – than ISG could do $15.16 billion in sales in the quarter.

For the first time in its history, Dell’s systems business will be larger than its PC business in Q4. If you do the math given sales of $29 billion at the midpoint of a $28.5 billion to $29.5 billion forecast range for the whole company, then PCs will only drive around $13.8 billion if Storage comes in a $4.16 billion.

Dell reiterated its guidance that it would being in somewhere between $101 billion and $105 billion in fiscal 2026, up 8 percent. For the full year, CSG will edge out ISG, but not by that much, with CSG coming in at about $52.3 billion and ISG generating $50.8 billion in our models. Dell may have the largest OEM system business during its F2026 year, but Nvidia’s datacenter will be somewhere around 3.5X as large, and a whole lot more profitable.

In the table above, for the sake of perspective, we have taken the quarterly revenues from AI servers and converted those sales into rough eight-way GPU nodes and then also figured out the amount of GPUs this might represent from those revenues.

As you can see, it doesn’t take very many GPUs at current street prices to drive the revenues for AI servers at Dell, or any other OEM or ODM, for that matter. We think Dell will resell somewhere around 260,000 GPUs to drive that $15 billion in AI sales in F2026, which is a factor of 8.4X in iron compared to F2024. But, over that same time, ISG revenues will have grown by 1.5X and operating income will have only grown by less than 1.4X in our model.

AI supercomputing is really supercomputing – sales go up and down wildly, driven by a few very demanding customers, there is a hope for widespread mainstreaming of the technology, and it is hard to make a profit.

Sign up to our Newsletter

Featuring highlights, analysis, and stories from the week directly from us to your inbox with nothing in between.

Subscribe now