Marvell Technology made some big bets about delivering chip packaging and I/O technologies to the hyperscalers and cloud builders of the world who want to design their own ASICs but who do not have the expertise to get those designs across the finish line into products. And this has absolutely turned the company’s fortunes around in a way that buying into the Arm server CPU and hyperscale networking businesses did not pan out.

But perhaps expectations are getting a little ahead of the practicalities of having Amazon Web Services and Microsoft as the lead partners for Marvell’s chip shepherding business. Which is really a problem that Wall Street has more than it is a problem that Marvell has. And, of course, Marvell is whipsawed around like all other semiconductor companies as the trade war between the United States and the rest of the world messes up supply chains and economic forecasting for everyone.

In the quarter ended on May 3, which is the first quarter of Marvell’s fiscal 2026, Marvell had just under $1.9 billion in sales, a record for the company and up 63.3 percent year on year. This was the second straight quarter of operating income in the black after seven prior quarters of being in the red (and sometimes deeply), with middle line hitting $270.6 million, up 13.1 percent sequentially, but with the bottom line down 12.5 percent sequentially to $177.9 million.

Marvell ended the quarter with $886 million in cash and equivalents and $4.23 billion in the bank, and has just closed a deal to sell its automotive electronics business to Infineon this year for $2.5 billion, which will give Marvell the cash it needs to be a supplier of chip services to the hyperscalers and cloud builders.

The company said on its call with Wall Street analysts that it was forecasting second quarter of fiscal 2026 sales of $2 billion, give or take a little, which is a smidgen better sequentially and 57 percent growth year on year, a little slower than this quarter.

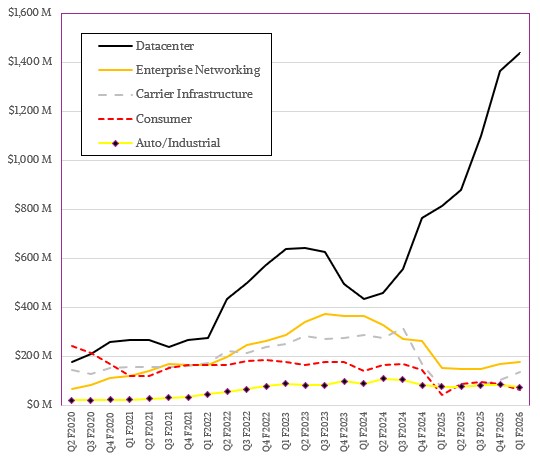

Marvell’s datacenter business, like that of Nvidia, utterly dominates its financials at this point, and that is largely due to chip shepherding deals with Amazon Web Services for Trainium and Trainium 2 AI processors and Microsoft Maia AI processors. There has been speculation for the past year that Marvell might be losing the AWS XPU business to Alchip Technologies, a chip design and packaging firm based in Taiwan that is also, like Marvell, an early adopter of Nvidia’s NVLink Fusion IP blocks to add NVLink ports to custom accelerators.

“Our lead XPU program for a large US hyperscale datacenter customer is doing extremely well and has become a key revenue driver for our custom business,” said Matt Murphy, Marvell’s chief executive officer, on a call with Wall Street analysts. “I am incredibly proud of our team and the close collaboration with this customer to drive this program to volume production with A0 silicon and meet the customer’s steep ramp. As I mentioned last quarter, we are fully engaged with this customer on the follow-on generation and I’m pleased to report that we have now secured 3 nanometer wafer and advanced packaging capacity and expect to start production in calendar 2026. At the same time, our architecture team is working with the customer to support the definition of the generation after that.”

This customer is AWS, and Murphy is referring to the Trainium 2 in production, the ramp for Trainium 3, and the specs for the future Trainium 4.

Murphy added that the design win it got for a next-generation AI XPU from another US hyperscaler, widely believed to be Microsoft with its Maia 100 chip, “continues to progress well” and that the company is already engaged with the same customer on a follow-on AI XPU, which we might call the Maia 200 in the absence of a real name from Microsoft.

Marvell is hosting an AI event on June 17, and we hope to get more insight then on what it is doing and what plans it has to grow this business further. And to get more details on second sourcing of chips by these hyperscalers, which is something Murphy admitted could happen in the call given the volumes that these customers want to get into the field. Perhaps Alchip and Broadcom will get pieces of this AWS and Microsoft action as yet. . . .

Datacenter product revenues, which include custom XPUs as well as custom compute and various kinds of optics, added up to $1.44 billion in fiscal Q1, up 76.5 percent year on year and up 5.2 percent sequentially. Enterprise networking, which includes the combination of Prestera and Innovium switches and network interface cards, rose by 15.9 percent to $177.5 million. The datacenter and enterprise networking businesses comprised 85.4 percent of total revenues for the company, showing just how small these other businesses now look as has happened to Nvidia and to a lesser extent to AMD. These are datacenter companies that now dabble in other areas.

Marvell did not give much in the way of specifics about its AI revenues and how it all broke down across XPUs and networking. But we had pretty good data in the prior quarter, and we took a stab at extrapolating it for Q1 F2026.

We reckon that overall AI revenues were $912 million, or about 63.3 percent of datacenter revenues, up 3.7X from the year ago quarter. In our model, AI XPU revenues rose by 2.6X to $291 million, but AI electro-optics drive $621 million in sales, up 4.5X year on year. That puts AI revenues at just under half of total revenue for the entire company, and we do not think it will be long before more than half of Marvell’s sales come from its products and services aimed at the AI market.

Which stands to reason. AI is driving the other half of an expanded IT market now.

Sign up to our Newsletter

Featuring highlights, analysis, and stories from the week directly from us to your inbox with nothing in between.

Subscribe now