Meet The Company Challenging Nvidia's AI Dominance. (Hint: It's Not AMD) | The Motley Fool

作者:Keithen Drury

Broadcom's custom AI accelerators are gaining momentum.

Nvidia (NVDA 3.90%) has been the undisputed king of artificial intelligence (AI) investing. Its products have been used to train and run AI models from the start, and they are still the computing unit of choice for many AI hyperscalers.

However, there's a rising competitor that's starting to gain a lot of traction with these giants. It's not AMD (NASDAQ: AMD), as its products are very similar to Nvidia's. Broadcom (AVGO -1.57%) is a rising player in this field, and it's doing it with custom chips that are designed in collaboration with the end user. This makes for a different business model than Nvidia is currently using, and it could challenge Nvidia's AI supremacy over the next few years.

Image source: Getty Images.

Broadcom's custom designs can replace Nvidia GPUs in some applications

Nvidia makes graphics processing units (GPUs), which are great for any task that requires significant computing power. GPUs can process multiple calculations in parallel, an effect that can be amplified when hundreds or thousands are connected in computing clusters. GPUs are useful for many other workloads outside of artificial intelligence, as they're also used for gaming graphics, engineering simulations, drug discovery, and mining cryptocurrency. Because of their varied use cases, GPUs are designed to be flexible for whatever application they're being deployed for.

Nvidia's GPUs are best-in-class, and with AI hyperscalers sparing no expense to make the best AI model possible, Nvidia's GPUs are the number one choice. But what if these GPUs will only see one type of workload during their service life? Then, all the extra features that make GPUs flexible for whatever workload they'll see become useless. That's where Broadcom's custom AI accelerators come in.

Broadcom is collaborating with the end users to design chips that meet their needs, which allows them not to buy as many Nvidia GPUs. These application-specific chips aren't flexible like GPUs, and they are really a one-trick pony. But that one trick allows them to outperform GPUs because there isn't a need to pay for extra features. Furthermore, Broadcom is working with the end users rather than selling them a complete product, so the customer doesn't need to pay a massive premium like they do with Nvidia chips.

This could lead to a massive market opportunity and allow Broadcom to challenge Nvidia's dominance over the long term. But just what kind of upside can investors expect?

Broadcom's stock has received a premium from the market

The market is well aware of Broadcom's rising dominance. The stock popped by nearly 10% after it revealed that it had a new customer for its XPUs (what it calls its custom AI accelerators) that placed a $10 billion order during the quarter. That adds to the incredible run Broadcom's stock has been on, as it's up over 50% this year.

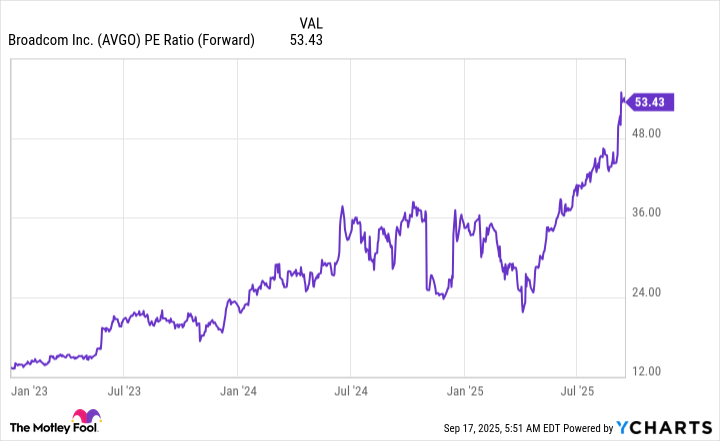

However, the stock is starting to get expensive due to all of the excitement surrounding Broadcom's growing AI business. Broadcom now trades for 53 times forward earnings, which is far more expensive than its peer, Nvidia, which trades for 39 times forward earnings.

AVGO PE Ratio (Forward) data by YCharts

However, that premium is warranted. Broadcom's AI revenue grew 63% year over year in Q3 of fiscal year 2025 (ended Aug. 3) to $5.2 billion. That's faster than Nvidia's Q2 of fiscal year 2026 (ended July 27), which saw revenue rise 56% to $46.7 billion.

That's a significant revenue total mismatch, and it should be noted that Broadcom does a lot more than just custom AI accelerators. Within its AI division are networking witches for data centers, which are used regardless of whether its custom AI accelerators are deployed or if a client is using Nvidia GPUs. Additionally, Broadcom has a lot of other business units, which slow down its overall growth rate. Companywide in Q3, Broadcom's revenue rose 22% year over year to $16 billion.

So, Broadcom still has a way to go before becoming the next Nvidia. However, with its custom AI accelerators picking up momentum, I think 2026 could be an incredible year for the company. The stock has already gained a ton in anticipation of this rise; now it's up to Broadcom to deliver on the hype it has created around itself. I don't think investors need to sell their Nvidia shares quite yet, but they should keep an eye on Broadcom's AI growth relative to Nvidia's to understand how each is faring.

Keithen Drury has positions in Broadcom and Nvidia. The Motley Fool has positions in and recommends Advanced Micro Devices and Nvidia. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.