AI 2025的状态

作者:Christine Deakers

如果2023年是AI大爆炸*,那么2025年就会感觉像第一光。早期灾难的雾气揭示了基础公司的集群,建筑的最佳实践以及创业成功的模式。我们仍然是宣布任何稳定性的方法,但是这些AI星系比以往任何时候都更了解即将到来的事物。

我们首先应该明确指出,我们非常有信心AI正在推动我们见过的最大技术变化。创始人想知道如何在风险投资张开嘴时如何将炒作与现实分开,但是在AI的情况下,简单的数字讲述了这个故事。如果最直接的启动现实度量是收入增长,那么我们更新了基准并专注于20个惊人的AI初创公司,以帮助定义一家出色的AI初创公司的外观。尽管这些基准无疑会在未来几年发展,但很明显,在Saas时代,构成一家出色的创业公司的原因不再削减了。

没有AI就没有云。

当然,AI时代并不为初创企业和投资者带来统一的好消息。

一些增长信号可能会产生误导。买家饿了,AI演示令人眼花naz乱,销售可能会飙升,但并非所有产品都具有真正的价值。保留可能很脆弱,尤其是当切换成本低时。仅早期超增长就意味着现在比以往任何时候都更少。

大爆炸很难忽略,因此竞争强度是历史最高的。有前途的地区吸引了2次3倍的竞争对手。最重要的是SaaS巨人正在醒来对于包括我们投资组合中的许多人的AI命令,例如已经推出了1亿美元+ AI产品的对讲机。我们怀疑这些领导人将在未来几年提供竞争压力(以及并购的诱惑!)。

我们还在疯狂的不可预测性时刻。我们的头可能今年旋转的速度可能会稍慢一些,但它们仍在旋转。在模型上下文协议(MCP),AI浏览器以及许多其他领域中,我们将在本报告中标记的含义仍然使我们挠头,只有模糊地猜测了该AI宇宙的部分如何发展。

但是,可以肯定的是。没有AI就没有云。

在Bessemer,自2023年我们最初的承诺以来,我们已经将超过10亿美元的资本部署给了AI-Native创业公司。此外,从本质上讲,每个传统SaaS公司都在利用AI的产品和运营中。无论我们是否能够完全能够浏览这个新的AI宇宙,我们现在都在其中。

在此AI报告中,我们的目标是:

- 分享我们的最新消息基准对于伟大的AI初创公司的样子

- 参观我们的路线图跨基础架构,开发人员工具,水平AI,垂直AI和消费者,同时突出显示稳定的星系在星座形成的每个空间中

- 表面暗物质 - 重要的领域,有重大问题

- 提供我们的五个预测对于我们期望在一两年中看到的东西。

随后的AI宇宙的模糊地图是针对可以容忍航行规则实时重写的航行的初创旅行者。前面的旅程可能会颠簸,但至少不会很无聊。我们在这里为此。让我潜水。

*关于真正的AI Big Bang的辩论仍在持续到2012年深度学习中的Alexnet突破。其他人遵循Openai的2020缩放法律。对于本报告,我们将Chatgpt的大规模释放视为AI真正爆炸为公众意识的那一刻。

AI基准:伟大的初创公司在2025年的样子

基准一直是判断初创企业的一种不完美的方式,但是在AI时代,它们的可靠性也不太可靠。特别是,一些AI初创公司已经实现了世界从未见过的增长率,驱使每个AI创始人想知道好的外观。因此,我们更新了我们的基准,即某些AI初创公司正在玩不同的游戏。

两个AI初创公司和新T2D3的故事

为了制定我们的新基准测试,我们研究了20个高增长,耐用的AI初创公司,包括突破困惑,,,,删节, 和光标。一个

尽管所有这些AI明星都表现出惊人的增长,但仔细研究清楚地表明,在AI时代,有两种不同类型的惊人类型:超新星和流星。

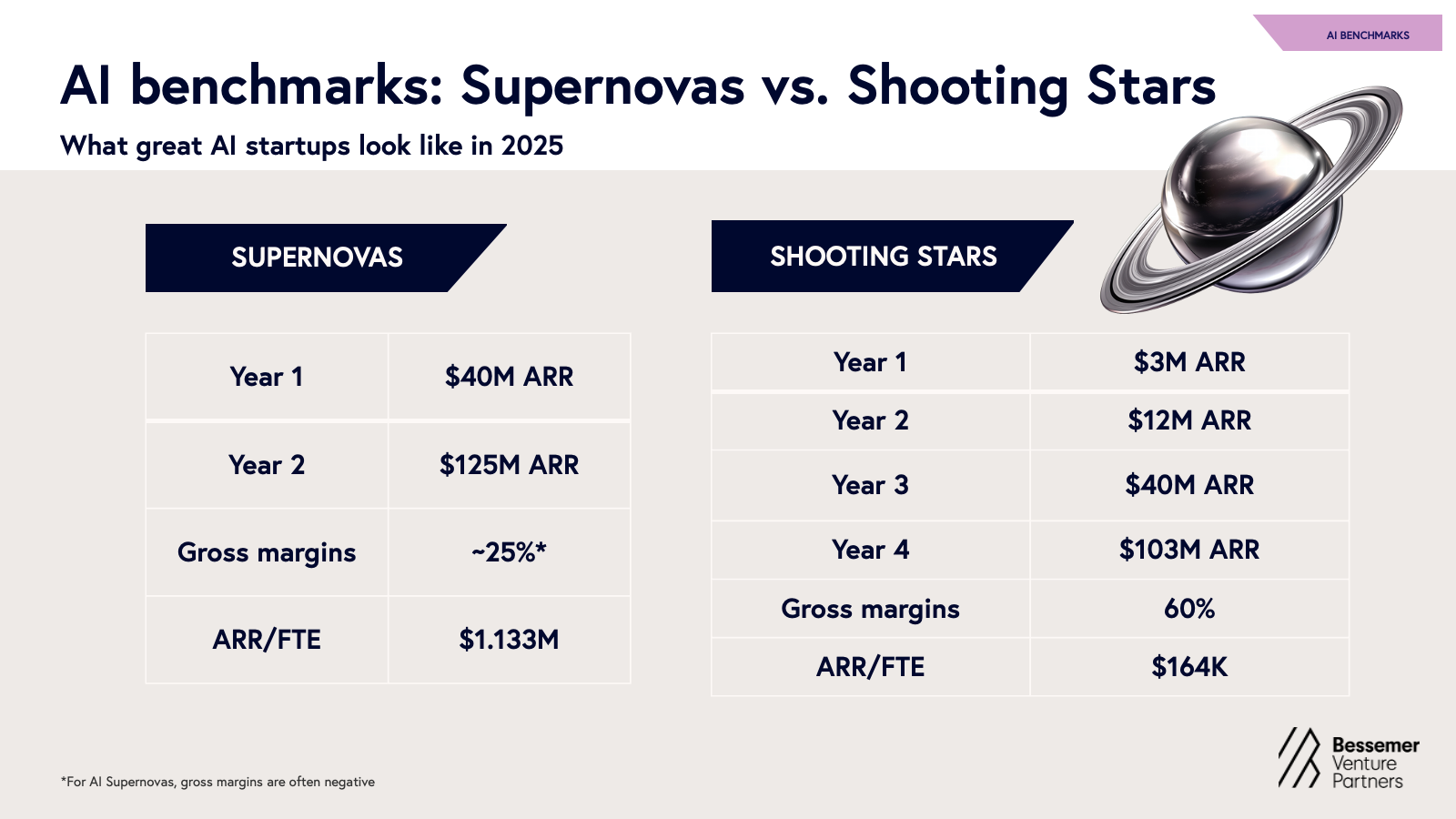

AI超新星

Supernovas是AI初创公司在软件历史记录中的生长速度。这些企业通常会在商业化的第一年中立即从种子上升至1亿美元的ARR。这些都是我们看到的最令人兴奋和最恐怖的创业公司。几乎从定义上讲,这些数字是由于收入可能显得脆弱的情况而产生的。它们涉及快速采用,即掩盖了较低的开关成本,或者表明可能与长期价值不符的大量新颖性。这些应用通常与核心基础模型的功能如此接近,以至于可以抛出薄包装器标签。在红热的竞争空间中,由于初创企业使用每种工具来争取获胜者奖品,因此利润率通常接近零甚至负面。”

我们调查的十家AI超新星初创公司在商业化的第一年达到了约4000万美元的收入,在收入的第二年中,ARR约为1.25亿美元。当然,Topline ARR并不能保证健康的业务。可持续增长取决于强大的保留,参与和资本效率。这些AI超新星平均只有25%的毛利率,通常在短期内以利润进行交易。尽管这些较低的利润率,这些AI超新星似乎表现出令人难以置信的113万美元ARR/FTE,它比典型的SaaS基准高4-5倍。这种收入效率可能表明对非常有效的业务的长期潜力。

| 超新星:以前所未有的增长和采用来爆炸性地扩展AI初创企业。 | ||

| 平均基准 | 1年级 | 2年级ARR |

| 年度经常性收入 | 4000万美元 | 1.25亿美元 |

| 一个 | 平均的 |

| 毛利率 | 〜25%(通常为负) |

| 一个 | 1年 |

| arr/fte(平均) | 11.3万美元 |

AI射击星

相比之下,流星看起来更像是出色的SaaS公司:由于更快的增长和适度的模型相关成本,他们发现产品市场迅速合适,保持和扩大客户关系,并保持较高的毛利率略低于SaaS同行。它们的平均生长速度比SaaS的前任更快,但是以仍感觉到扩展组织的传统瓶颈的速度。这些业务可能尚未主导头条新闻,但它们受到客户的喜爱,并且正在轨迹上制作软件历史记录。

平均而言,这些流星在收入的第一年内达到了约300万美元的ARR范围,而Yoy增长的三倍,最初几年约60%,ARR / FTE约为$ 164K。

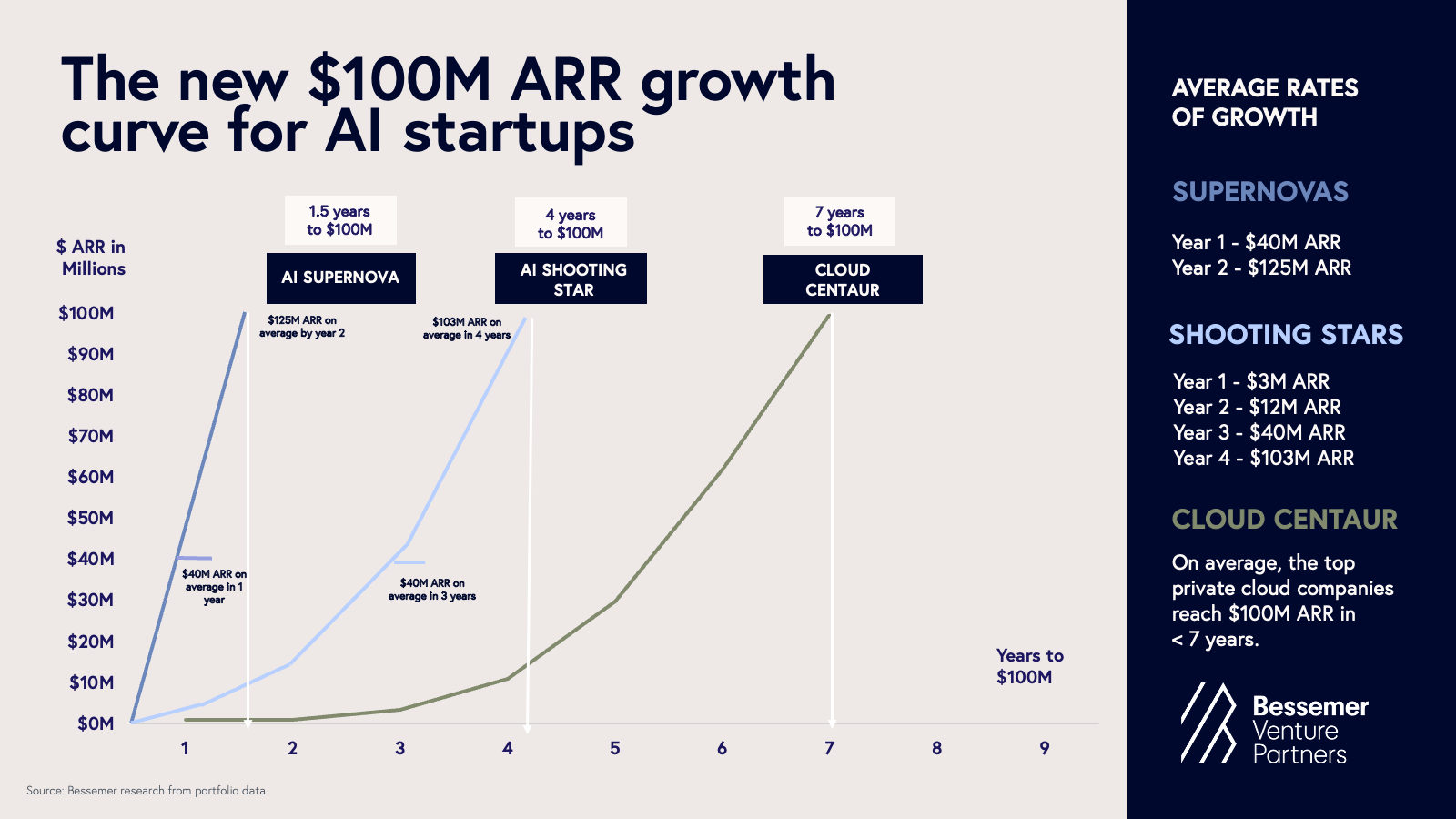

如果T2D3(三,三,双,双,双,双重)定义了SaaS时代,则Q2T3*(四倍,四倍,三倍,三倍,三倍)更好地反映了我们从今天的SAI Shiph Stars中看到的五年轨迹。这些初创公司的生长速度比传统的SaaS更快,但仍然比SaaS基准比爆炸性AI超新星更接近SaaS基准。

虽然我们喜欢超新星,但我们相信这个时代将不是几个异常值来定义的,而是由数百名流星定义。这使得Shower Stars成为AI创始人目标最重要的基准。

| 流星:快速增长的,资本效率高的AI初创公司具有强大的PMF,可靠的利润和忠实客户的规模,例如Stellar SaaS。 | ||||

| 平均基准 | 1年级 | 2年级ARR | 3年级ARR | 4年代arr |

| 年度经常收入 | 〜300万美元 | 〜1200万美元 | 〜4000万美元 | 〜1.03亿美元 |

| 一个 | 1年 |

| arr/fte(平均) | 〜$ 164K |

这些新基准的AI创始人的关键要点: 我们公认分享这些怪异新的基准测试以展示当下杰出的AI初创公司的现实。也就是说,建立一家标志性的AI公司不需要一夜之间进行四倍。许多最强大的公司仍将采取更加故意的道路,这是由产品复杂性和竞争动力所影响的。

但是,速度比以往任何时候都重要。AI已解开了更快的产品开发,GTM和分销,使Q2T3(四倍,四倍,三倍,三倍,三倍)取消了雄心勃勃的但越来越可实现的基准。数十家初创公司已经证明了这是可能的,我们相信您也可以!

*诚然,我们还没有看到五年的数据,所以也许在未来的几年中,我们会知道这些公司的真正三倍,但是Q2 T1 D2几乎没有吸引力。”

AI Cosmos的路线图

在Bessemer跟踪的每一个路线图中,我们看到了过去一年中AI堆栈的许多元素,从而形成了几个早期星系。我们将在每个路线图中调查这些星系,同时指出“暗物质”的许多区域,我们仍在猜测未来的情况。

I. AI基础设施

星系形成:模型层

让我们从显而易见的开始:少数球员,例如Openai,Anthropic,Gemini,Llama和Xai继续主导着基础模型景观,推进了模型性能,同时探索了垂直集成。现在很明显,大型实验室正在不提供仅提供基础模型和模型开发的工具 - 这些实验室现在正在推销用于编码,计算机使用和MCP集成的代理。同时,由软件创新和端到端硬件优化驱动的计算成本继续下降。”

诸如Kimi,DeepSeek,Qwen,Mixtral和Llama之类的最先进的开源模型也继续证明,开放的生态系统仍然可以超过其重量,通常在效率和专业任务中匹配或超过专有模型。

在研究方面,我们看到了一波创新:Google最近混合回收纸以适应性深度的方法来平衡推理吞吐量和少量准确性。专家架构的混合物也通过新技术来恢复,以将专家以独特的方式相结合。最后,诸如测试时间增强学习(RL)和自适应推理之类的推理时间技术正在增强,垂直领域可能会看到一些最重要的突破。

这些模型级创新只是较大的替补的一部分。

随着公司建造AI-NENITAIDE和AI-IMBEDDED产品,新的基础设施层出现了跨越模型,计算,培训框架,编排和可观察性。我们在我们的AI基础设施路线图从2024年开始。这个专业的堆栈为建筑商提供了所需的速度和灵活性,但是随着玩家进入邻接以拥有更多堆栈的捆绑,捆绑正在加速。尽管到目前为止取得了惊人的进步,但我们认为AI基础设施的快速发展还远远没有结束。

AI基础设施的第二幕

AI的第一个时代是由主要的算法突破,卷积网络,变形金刚定义的。该领域主要通过算法改进和缩放方法提出。因此,基础设施反映了这种心态,从而推动了巨人在基础模型,计算能力和数据注释等领域的兴起。

但是下一章可以证明更深刻。

作为Openai的Shunyu Yao最近观察到,现在AI的下半年将把重点从解决问题转移到定义问题上。

在AI基础设施的第二幕,该行业将从证明AI可以解决问题到定义,衡量和解决经验,清晰度和目的的问题的系统。

大型实验室正在超越追求基准增益来设计可以与现实世界有效互动的AI。同时,企业正在从概念证明到生产部署毕业。

所有这些转变都为新一波的基础设施工具奠定了基础。一些示例包括:

- 强化学习环境和通过平台的任务策划例如舰队,,,,矩阵,,,,机械化,,,,凯森,,,,vmax, 和Veris,由于人类生成的标记数据不再足以实现生产级AI

- 新颖的评估和反馈框架例如bigspin.ai,,,,窑炉, 和审判实验室,启用连续和特定的反馈循环

- 复合人工智能系统不只是专注于原始模型马力,但结合了诸如知识检索,记忆,计划和推理优化之类的组件

我们正处于从AI作为概念证明向AI的过渡开始,作为一种嵌入现实世界经验中的解决问题和适应性系统。

暗物质:ai的痛苦教训

里奇·萨顿(Rich Sutton)痛苦的教训提醒我们,AI中最有效的进步历史上是利用计算和通用学习,而不是依靠手工制作的功能或人为设计的启发式方法。随着AI基础架构进入下一章,随着从业者寻求嵌入上下文,理解和领域专业知识以确保现实世界实用性,这仍然是一个开放的问题。

形成星系:AI工程是软件开发不可或缺的一部分

除了基础架构堆栈之外,AI明显改变了软件开发。自然语言已成为新的编程接口,并在指令上执行模型。在此范式转变中,由于提示现在是使用LLMS作为新型计算机的提示,因此软件开发的原理正在发生变化。

AI并不意味着开发人员工具的增量演变,它已经迎来了一种全新的软件开发方式。我们将在即将到来的路线图中详细介绍此景观,用于软件3.0的开发人员工具(订阅地图集首先。)

如今,问题不是您的团队使用AI,而是您将其编排成更复杂的高速系统。这种软件开发模式感觉就像是ai-native开发的星系。最好的工程团队只是用AI编写代码,它们会在每个周期中更快地学习,适应和运输的系统。

形成星系:模型上下文协议(MCP)

新的基础设施将对AI发展产生深远的影响模型上下文协议(MCP)。由人类引入在2024年底,Openai,Google DeepMind和Microsoft迅速采用了MCP,成为代理商访问外部API,工具和实时数据的通用规范。

正如MCP创建者所描述的那样,可以将其视为AI的USB-C。它支持持续的内存,多工具工作流以及跨会议的粒度许可。有了它,代理可以链接任务,通过实时系统进行推理,并与结构化工具进行交互,而不仅仅是生成输出。

对于开发人员,MCP从根本上简化了集成。对于创始人来说,它为建造真正的代理产品打开了大门,而AI不仅可以帮助用户,而是代表他们跨系统的行动。还要早,很重要的是要注意MCP是一本食谱书,而不是厨师。为了真正做饭,我们需要像FastMCP从长官(这使得构建MCP服务器变得更加容易)和类似的工具拱廊和钥匙卡(这有助于代理授权和许可。)随着星座继续围绕MCP连接器,治理框架和特定于代理特定的工具形成,我们希望它能像HTTP一样成为Internet的代理本地网络的基础。

暗物质:记忆,上下文及以后

随着AI本地工作流的成熟,内存正成为核心产品原始产品。跨时间记住,适应和个性化的能力是将工具从有用的到必不可少的。出色的AI系统正在扩大过去的召回和用户的发展。在2025年,大的上下文窗口和检索型发电(RAG)使更连贯的单会互动使得真正持久的跨主题记忆仍然是一个开放的挑战。虽然基础模型公司正在研究内存,但类似的初创公司也是如此MEM0,,,,Zep,,,,超级记忆和langmemLangchain。一个

上下文是模型在推断过程中看到的数据。内存是指在支持多步推理,个性化和代理连续性的交互中保留的信息。他们共同为下一代AI应用程序提供动力。

我们认为,领先的堆栈最终将结合以下内容:

- 通过扩展的上下文Windows(128K至1M+令牌,取决于模型和体系结构)的短期内存(128K至1M+令牌)

- 通过向量DB,记忆OS(例如备忘录)和MCP风格的编排的长期记忆

- 通过混合抹布和新兴情节模块的语义记忆,旨在富裕的回忆

尽管如此,折衷仍然存在:长篇小说提高了潜伏期和成本。如果没有智能上下文工程的动态选择,压缩和任务隔离是关键的,持续的内存是脆弱的。

代理应用程序代理,客户副词,创意工具是领先采用多模式内存层和状态工作流程。同时,对神经记忆,持续学习和局部环境缓冲区的研究表明,可扩展的召回已达到范围。

对于AI应用程序创始人,上下文和内存可能是新护城河。对于解决这些问题的建筑商而言,AI中的转换成本几乎可能会变得情绪激动。当您的产品比其他任何东西都更好地了解用户的世界时,更换的感觉就像是重新开始。无论是在您的团队代码库中流利的编码助手,还是嵌入CRM和通信堆栈中的销售代理,对用户的累积智能及其特定环境都成为最具困难的资产。

仍然存在许多未知数,但是获胜的初创公司可能需要掌握基础架构和未来的界面:

- 构建具有低延迟召回的灵活的记忆感知系统

- 设计隐性学习和与核心工作流程的深层集成

- 将上下文变成跨数据,分发和喜悦的复杂优势

创始人应该将记忆视为后端管道,而应将记忆视为产品。今天以记忆意识建立的初创公司将塑造明天最聪明,个性化和粘性的AI系统。

iii。水平和企业

形成星系:压力下的记录系统

在Enterprise软件中,AI开始为初创企业揭示破坏一些最大的记录水平系统(SOR)的机会。几十年来,Salesforce,SAP,Oracle和ServiceNow之类的SOR凭借其深厚的产品表面,实施复杂性以及对业务关键数据的中心地位而保持坚定。企业享受了软件中一些最强的护城河。切换成本太高了,很少有创业公司甚至敢于尝试并取代它们。现在,那些护城河正在退化。

凭借AI构建非结构化数据并按需生成代码的能力,迁移到新系统的速度比以往任何时候都更快,更便宜且更可行。代理工作流程正在替换死记硬背的数据输入,并且需要系统集成商军队的典型实施项目和数年的工作量通过数量级加速。

这些新平台不只是存储信息。CRM工具day.ai和阿提奥通过电子邮件,通话和松弛的自动驾驶客户互动。ai本地的ERP珠穆朗玛峰,,,,道斯和里尔,自动化财务预测和采购流动。生产力达美越来越不可能忽略。创始人不再只是构建更好的记录。”他们建立了行动系统。

建立行动系统的创始人的关键解锁是什么?

- AI Trojan Horse特征:使创业公司能够使用有价值的楔形工具来利用数据流,该工具使他们能够开始捕获所有流入记录系统的数据,而无需在第一天将其删除

- 实施:使用CodeGen工具和AI将自然语言中描述的业务逻辑转换为代码的能力更快90%

- 数据:自动化,利用AI在不同的模式之间翻译,实现1天数据迁移的能力,使历史供应商锁定几乎过时了

- 投资回报率:10倍与遗产,而不仅仅是增量;代理工作流减少专业服务的支出并加速到价值的时间

我们认为我们正在从纪录系统转向行动系统的一代转变开始。

形成星系:下一代CRM,人力资源和企业搜索

最大的问题是:AI-Native挑战者是创建Net-New类别吗?或者最终威胁到现任者?在CRM中,早期的破坏迹象很有希望。这些工具仅取代了现有的CRM,它们提供了一种新的体验。他们同时从销售团队中卸载了大量的手动工作,这也为销售经理提供了明智的建议,以根据所有渠道上的自动合成交易信号在哪里度过时间。这是一个10倍的飞跃,而不是10%的进步。

我们看到类似的楔子:

- 人力资源和招聘:用于候选筛查,入职和性能跟踪的AI副驾驶

- 企业搜索:接受内部知识训练的水平副驾驶正在扮演以前被SharePoint或Intion搜索担任的角色

- FP&A:AI本地FP&A工具允许财务分析师从许多不同的孤岛中集中数据,并在其上进行复杂的分析,而无需支持数据工程团队

真正的力量移动?从AI楔形的相邻,高价值的能力开始,然后逐渐扩展为完整的记录系统。这使挑战者可以随着时间的推移收集专有数据,同时仍然可以很好地与旧的工作流进行效果。公司喜欢贸易空间在IP管理或服务在ITSM中是这种方法的好例子。

现在仍然很早就开始了,但是在Net-New类别和真正的SOR更换之间开始形成清晰的战线。这将是一个有趣的观看空间。

暗物质:企业ERP和记录系统的长尾巴(SOR)

尽管有所有势头,但一些最大的企业表面仍然令人惊讶地不足:

- 企业量表ERP:尽管我们通过AI-Native会计和ERP平台看到了大量令人兴奋的活动,但当今大多数人都专注于SMB和中型市场客户,在很大程度上是在软件和服务等领域中比具有高度复杂的制造,供应链,供应链和库存要求的行业更简单的。也就是说,我们认为AI可以在这些更复杂的环境中提供巨大的价值,但是新进入者需要花费一些时间来建立为像这样更复杂的客户提供服务所需的产品的广度,并且我们认为真正的企业ERP替换周期仍然存在很多年。

- Sor的长尾巴:尽管CRM和ERP在记录系统方面引起了很多关注,但记录系统的尾声更长,这也代表了随着时间的流逝而大大的破坏机会。这些范围从企业安全中的身份平台到公共安全的计算机辅助调度系统到网络设计中的内容管理系统。我们认为所有这些类别都是破坏的成熟,但这是一个长达十年的旅程,企业家刚刚开始将注意力转移到这些类别上。

诺言是巨大的,但执行仍然难以捉摸。当我们看2026年时,我们认为下一波恒星可能诞生在这些空间中,但仍然为时过早。

iv。垂直aiâ

去年,我们提出了一个大胆的论文:垂直AI即使是最成功的传统垂直SaaS市场也有可能蚀。我们对这一论文的信念比以往任何时候都更加强大。收养继续加速,特别是对于长期以来一直是手动,服务繁重或对技术具有抵抗力的垂直工作流程。这重塑了我们对所谓的技术恐惧症垂直的看法。实际上,这个问题从来都不是缺乏采用新工具的意愿,正是传统的SaaS未能解决多模式或语言沉重的高价值垂直特定任务。垂直AI终于会与这些用户会面,而这些用户的感觉不像软件,而更像是真正的杠杆作用。

形成星系:垂直特定的工作流程自动化

多个行业,令人惊讶的是,许多在过去的时代被认为是技术恐惧症的行业都表现出有意义的垂直AI采用的明显迹象。例如:

- 卫生保健: 删节使用生成的AI自动化临床笔记,缓解提供商的倦怠,同时提高文档质量。Smarterdx通过自动化复杂的编码工作流程,帮助医院恢复了错过的收入。开放式自动化医学文献审查并在护理点上提供即时答案。

- 合法的: 均匀通过产生合法的需求套餐,将手动工作的几天变成了几分钟,允许审判律师和人身伤害公司扩展案件。ivo帮助法律团队自动化合同审查并在业务中跨合同进行自然语言搜索。Legora加速法律研究,审查和起草,同时在整个工作流程中进行协作。

- 教育:诸如轻快的教学和Magicschool为教师提供AI驱动的工具,以简化等级,辅导和内容创建等任务。

- 房地产: Eliseai从前景和居民通信到租赁审计,可以自动化以前的劳动密集型手动财产管理工作流程。

- 家庭服务: 孵化充当AI驱动的客户服务代表(CSR)团队。里拉使用现实世界的音频,大规模指导代表代表代表销售对话进行分析。

我们看到有关突破公司如何处理这些垂直领域的清晰模式:

- 引人入胜的楔子:早期的获奖者首先要解决一个核心疼痛点,该核心痛点通常是较重的或多模式的,因此,以前的软件浪潮服务不足。最好的楔入产品是直观的,并且经常嵌入现有的工作流中,以使收养无缝。语音/音频一遍又一遍地出现,这是一个奇迹般的楔子的常见方面。

- 上下文是关键:防御性源于领域专业知识:为垂直特定需求而建立的集成,数据护城河和多模式界面。最强大的团队迅速超越了微调,并进入了深层的垂直实用程序。

- 为价值建造:从第一天开始,ROI就很清楚,没有Excel电子表格需要向用户解释。这些工具解锁了10X生产率,将劳动力重新分配到高价值工作,降低成本或推动一线增长。价值是直接的,不是一个好。

暗物质:垂直AI中的问题

在所有动力上,在三个关键领域的垂直AI中仍然存在真正的未知数:

- 与记录遗产系统的互动:下一代垂直AI公司是否会继续与现有记录系统(今天的现状)的实用性集成并扩展或直接与它们竞争?Could we see a future where these legacy systems of record are no longer central at all, and are instead replaced by AI-native, vertical-specific systems of action?

- Competition from incumbents:In verticals where entrenched incumbents are not sleeping at the wheel, will scale and distribution win out over upstart innovation, or will a new generation of companies break through despite the odds?

- Sustainable data moats:As Vertical AI companies expand their scope, can they maintain meaningful data advantages in industries where data is fragmented, privacy-sensitive, and often difficult to access or standardize at scale?Â

V. Consumer AIÂ

As the underlying technology evolves, so do opportunities to tap into new consumer needs.Last year, most consumer usage leaned toward productivity-driven tasks, such as writing, editing and searching, as consumers explored the novelty and utility of AI.But we’re starting to see a shift toward deeper use cases, including therapy, companionship, and self-growth.AI is no longer just a tool for task assistance, it’s poking into more meaningful areas of consumers' lives.

Galaxies forming: AI assistants for everyday tasks and creation

Consumers across age groups are increasingly turning to general-purpose LLMs, particularly ChatGPT and Gemini, for daily or weekly assistance (with an估计的600M and 400M weekly active users as of March 2025, respectively.) What began as a novelty has become a habit, with these tools now serving hundreds of millions of users each week.Even as a long tail of specialized apps emerges, most consumers continue to rely on these general assistants for a wide range of needs, including research, planning, advice, and conversation.

Over the last year,嗓音 emerged as a powerful modalityfor how consumers interact with these applications.Unlike legacy assistants like Alexa or Siri, LLM-powered voice AI can handle open-ended questions, facilitate reflection, and support more fluid, conversational exchanges, providing an intuitive, hands-free way to interact with technology.Platforms likevapiin the Voice AI space are helping power consumers’ abilities to interact with machines in a way that spans language, context, and emotion.Â

Perhaps one of the most meaningful shifts is in how consumers search for information and interact with the web altogether.In this evolving landscape,困惑has emerged as a breakout darling.Its model-agnostic orchestration and blazing-fast UX have made it a go-to for AI-native search.With the launch of Comet, Perplexity’s agentic browser, the company is pushing the frontier further, and it may well become the defining form factor for the next generation of agents that are ambient and proactive.

Beyond its emerging role as a superior assistant, AI is also lowering the barrier to creation turning every consumer into a potential creator.Consumers are building apps with tools likeCreate.xyz, Bolt, and Lovable, generating music withSuno和udio, producing multimedia with platforms such asMoonvalley,,,,跑道, 和Black Forest Labs,and accelerating ideation and iteration with tools likeFLORA, Visual Electric, ComfyUI和Krea.AI is transforming everyday consumers into creators, pushing the boundaries of what we once thought possible.Â

Galaxies forming: Purpose-built AI assistants

As consumers look to integrate AI more deeply into their daily lives, a wave of consumer applications has emerged to address specific needs.One of the fastest-growing areas ismental health and emotional wellness。While “ChatGPT therapy†continues to gain traction, we’re also seeing the rise of purpose-built tools centered on self-reflection and personal growth.This includes AI journals and mentors like玫瑰花蕾and gamified self-care companions like Finch, which help users set personal goals, build healthy habits, and track emotional well-being.Character.AI was an early signal of consumer appetite for emotionally expressive AI, but over the past year, that demand has gone mainstream, with LLM-powered tools increasingly designed to support long-term memory, emotional resilience, and self-development.

Another emerging category isemail and calendar workflows.A growing number of startups are trying to simplify scheduling, inbox management, and to-do list automation using AI.But because these are trust-sensitive use cases and competitive spaces with strong incumbents (e.g. Gmail), customer acquisition and retention has been a challenge.Â

While there is a raft of offerings across more niche consumer use cases like meal planning, fitness, and parenting, we’re less certain that clear winners will emerge in these niche spaces.Despite these options, most consumers still default to general-purpose LLMs, finding them “good enough†for many of these tasks.For specialized apps to break through, they’ll need to offer clear differentiated value with tailored experiences addressing sticky recurring use cases to justify a permanent place on a home screen.

Dark matter: Clear unsolved consumer pain points

Some of the most obvious consumer use cases remain underserved not due to lack of demand, but because they still require too much manual action on the user’s part.While early agentic products are emerging, the underlying technology is still maturing.

Questions around security, autonomy, and reliability remain unsolved, and so it’s still early days for agents that can take action on behalf of users.Â

Use cases hiding in plain sight begging for agent infrastructure to catch up include:Â

- 旅行:Travel booking remains fragmented and time-consuming.The opportunity for a personalized, end-to-end travel concierge is enormous, but still unclaimed.

- 购物:There is an opportunity for e-commerce to be fundamentally reshaped when the starting point is no longer Google but agents that handle browsing, price comparison, and even checkout on the consumer’s behalf.

Who will own these use cases?Will it be the player that controls the AI-native browser, the general-purpose LLM assistant, or a new wave of consumer, end-to-end agentic apps?The answer may determine the next generation of consumer platform winners.

Bessemer's top AI predictions for 2025

As with every year we surveyed our partners to determine our five most important predictions for AI in the years ahead.We whittled several dozen predictions down to these five that achieved at least some level of consensus.So without further ado:

1. The browser will emerge as a dominant interface for agentic AIÂ

As agentic AI evolves, the browser is emerging as a potential environment for autonomous execution—not just a tool for navigation, but a programmable interface to the entire digital world.

While voice will remain a natural modality for certain contexts, browsers offer something more powerful: an ambient, contextual surface embedded directly in daily workflows.Browsers integrate seamlessly into both consumer and enterprise systems, allowing agents to observe, reason, and act natively across the applications users already rely on.

The next generation of agentic browsers—like recently introduced Comet and Dia—will be much more than plug-ins.They will embed AI at the operating layer, enabling multi-step automation, intelligent interaction across tabs and sessions, and real-time decision-making.Unlike traditional extensions, these browsers can interpret user intent and execute workflows end-to-end.

We expect to see new AI-native browsers from OpenAI, Google, and others in short order, each pushing the boundaries of what agents can do in-session.The browser’s ubiquity, flexibility, and integration depth make it the most capable—and inevitable—interface layer for agentic AI across both B2B and B2C use cases.Let the new browser wars begin!

2. 2026 will be the year of generative videoÂ

2024 marked the mainstream inflection point for generative image models.2025 saw a similar breakout in voice, driven by improvements in latency, awareness, human-likeness, and customization, coupled with massive cost reductions.2026 is shaping up to be the year video crosses the chasm.Model quality—across Google’s Veo 3, Kling, OpenAI’s Sora, Moonvalley’s Marey, and emerging open-source stacks—is accelerating.We're nearing a tipping point in controllability, accessibility, and realism, that will make generative video commercially viable at scale.

Video has historically been the most expensive and complex medium.Generative video and multi modal models are collapsing these barriers, making video viable and accessible.We’re already seeing generative video models garner mainstream adoption across entertainment, marketing, education, social media, and retail.We expect a proliferation of startups and tools addressing specific use cases—from cinematic storytelling and avatar animation to real-time customer engagement and product videos.

We also expect the next 12 months to clarify the market structure for generative video:

- Do large labs win it all?Models like Google’s Veo 3 are setting the benchmark for video realism and control.希格斯菲尔德is making waves by building differentiated applications using in-context learning on top of existing frontier models—showing that you don’t necessarily need to train your own model to build a powerful product.

- Will open-source catch up?Unlike image generation, where open models have outperformed, video has had fewer open source leaders.Video models are compute and data intensive, costly to train and complex to evaluate.That said, we predict strong open video models will emerge in 2026—Qwen’s open video model is an early winner, and momentum is building.

- Are there advantages for real-time or low-latency use cases?We’re watching early teams like Lemonslice experiment with streaming video and real-time inference, where speed and responsiveness can become product moats in themselves.

There are a few top uses case we’re watching out for:Â

- Cinematic video: tools for creators, studios, and marketing teams, as with Moonvalley

- Real-time, low-latency generation: livestreaming, virtual influencers, gaming

- Extreme realism: photorealistic storytelling, virtual production

- Personalized content and social identity

- Developer workflows that make it easier to create video applications and outputsÂ

However, alongside technical progress comes growing complexity around IP.The copyright and regulatory landscape for generative video is still catching up asmajor studios are starting to take action against misuse of copyrighted assets.Startups operating in this space should be thoughtful and proactive about licensing data, sourcing training sets responsibly, and developing royalty structures that respect creators.This is not just about legal risk—it’s about long-term trust, differentiation, and defensibility.

Whether generative video becomes a few-player market dominated by the labs, or an ecosystem rich with apps, infrastructure, and open innovation, one thing is clear: a new era of video creation is here—and it's going to reshape the internet.

3. Evals and data lineage will become a critical catalyst for AI product developmentÂ

One of the biggest unsolved bottlenecks in enterprise AI deployment is evaluation.How is the product, feature, algorithm change “doingâ€?Do people like it?Is it increasing revenue / conversion / retention?Most every company still struggles to assess whether a model performs reliably in their specific, real-world use cases.Public benchmarks like MMLU, GSM8K, or HumanEval offer coarse-grained signals at best—and often fail to reflect the nuance of real-world workflows, compliance constraints, or decision-critical contexts.Â

That’s why 2025–2026 will mark a turning point:AI evals will go private, grounded, and trusted—and enterprise deployment will 10x because of it.Â

Today’s enterprises aren’t just seeking performance;they’re seeking信心。And confidence requires trusted, reproducible evaluation frameworks tailored to their own data, users, and risk environments.The shift is already underway: instead of chasing leaderboard scores, companies are buildinginternal eval suitesto measure how AI performs across privacy-sensitive workflows, customer support, document parsing, and agent decision-making.

This next era of AI measurement will be defined by:

- Private, use-case-specific evalsbuilt on proprietary data

- Business-grounded metricslike accuracy, latency, hallucination rates, customer satisfaction

- Continuous eval pipelinestightly integrated into production systems and feedback loopsÂ

- Lineage and interpretability,especially in regulated verticals like healthcare, finance, and insurance

Startups such asBraintrust,,,,Langchain,,,,Bigspin.ai和Judgement Labsare pioneering the infrastructure stack for this new era—offering eval harnesses, agentic benchmarking environments, real-time feedback loops, and more.

As enterprise buyers grow more sophisticated, they'll demand not just performance—but provable, explainable, and trustworthy performance.DataHubgives enterprises confidence that their AI models are only using the data from whom, for what and where it is supposed to, and provides lineage for additional verification and compliance.AI vendors will need to surface evidence of effectiveness before purchase, not just after deployment.In this context, evaluations and data lineage aren’t just development features—they become part ofa strategic layer of the AI stack,and a core requirement for procurement and governance. Â

Product development as we know it has always aspired to be data-driven and user-informed, with platforms like发射台enabling experimentation and measurement.In the world of AI—-where predictive versus deterministic user experience reign supreme, the very foundation of these product development principles has been rocked.Companies likeArklex,,,,Kiln AI和Pi Labspropose a radically new way of thinking about measurement and feedback loops in the AI-native era.Â

Founders building in this space should prioritize:

- Tooling for multi-metric evals(e.g., accuracy and hallucination risk and compliance)

- Synthetic eval environmentsfor stress testing agentsÂ

- Interoperability with logging, retrieval, and feedback systems

- Support for model drift and continuous updates over timeÂ

As foundational model performance converges,the real differentiator won't be raw accuracy—it’ll be knowing exactly how, when, and why your model works in your environment.The startups that can make evaluationscalable, explainable, and enterprise-readywill unlock the next wave of AI deployment—and define the next great infrastructure frontier.

Major shifts in consumer technology have historically paved the way for new social giants.PHP enabled Facebook.Mobile cameras made Instagram possible.Advances in mobile video propelled TikTok.It’s hard to imagine that the new capabilities enabled by generative AI won’t lead to a similar breakout.Â

We don’t yet know what form the next social media giant will take.It could be a network where AI agents quietly ensure we never miss a birthday, a friend’s update or an important event in our local area, helping us be our best selves online and IRL.Or it might be a world populated by emotionally intelligent AI influencers and AI clones.Platforms like Character.AI and Replika hint at social spaces where AI, not humans, could be the main characters.

Whatever shape it takes, breakthroughs in voice interaction, long-term memory, and image and video generation are clear fuel for the next social media breakout.The winning platform might launch with a mainstream splash or emerge from a niche community before rapidly expanding into a full-fledged ecosystem.

5. The incumbents strike back as AI M&A heats up

After two years of rapid disruption by AI-native startups, the enterprise giants are striking back—not by rebuilding from scratch, but by acquiring the capabilities they need to catch up.In 2025 and 2026, we expect to see a surge in M&A activity as incumbents move aggressively to buy their way into the AI era.

The battle lines are clearest in vertical software.As AI-native startups push deeper into industry-specific workflows—automating insurance claims, legal briefings, or revenue cycle management—traditional SaaS players face a stark choice: evolve or become obsolete.For many, the fastest path to innovation is acquisition.We anticipate a wave of consolidation in high-service, regulated industries like healthcare, logistics, financial services, and legal tech.

But this isn’t just about bolting on AI features.The rise of Vertical AI is forcing a structural shift—where the line between software and service blurs.AI tools are becoming so deeply embedded in domain workflows that they resemble intelligent service providers.For incumbents, acquiring these companies isn’t just an AI upgrade—it’s a reinvention of their value proposition.

At the same time, demand for AI infrastructure and tooling will drive strategic acquisitions in model orchestration, evaluation, observability, and memory systems.Enterprises aren't just buying applications—they’re buying the building blocks of an AI-native stack.

Takeaways for founders:

- Be ready for strategic interest: If you're building a domain-specific or infrastructure-layer AI product, expect inbound from legacy players looking to fill gaps.

- Play for leverage: The best-positioned startups will have strong technical moats, customer traction, and embedded workflows that make them hard to replicate.

- Know your acquirer’s roadmap: Understand where incumbents are falling behind in your space.If you can deliver what they can’t build fast enough, you’re valuable.

For investors, this wave of consolidation represents both liquidity opportunity and thesis validation: the incumbents are confirming—through their wallets—that AI-native companies are setting the new standard.The age of AI-native disruption may have started with startups, but the second act is underway—and the giants are suiting up.

The founder’s edge in the AI cosmos

We’re no longer at the dawn of AI—we’re deep in its unfolding galaxies.Today’s top startups aren’t just building faster software.They’re designing systems that see, listen, reason, and act—embedding intelligence into the fabric of work and life.

But here’s the truth: success in AI isn’t just about velocity.It’s about vector, as in speed in the right direction.The most iconic companies won’t be those who simply ride the wave, but those who shape it—aligning exponential capability with real-world clarity.

AI is no longer theoretical.It’s operational.It’s generating revenue, building relationships, and rewriting industry rules.And yet, much remains unresolved: memory, context, governance, agency.That’s the power of this moment—the map is still fuzzy, but the frontier is real.

Here are the top takeaways for AI application foundersÂ

- Two AI startup archetypes are winning:On average, Supernovas hit ~$100M ARR in 1.5 years—but often with fragile retention and thin margins;Shooting Stars grow like stellar SaaS: $3M to $100M over 4 years, with strong PMF and healthy margins.

- Memory and context are the new moats:The most defensible products will remember, adapt, and personalize.Persistent memory and semantic understanding create emotional and functional lock-in.

- Systems of action are replacing systems of record:AI-native apps don’t just store data—they act on it.Don’t bolt AI onto legacy software—reimagine the entire workflow.

- Start with an AI wedge:Solve a narrow, high-friction problem (e.g., legal research, sales notes).Deliver 10x value fast—then expand.

- The browser is your canvas:Agentic AI is shifting to the browser layer—now a programmable environment where agents observe and execute.Build for this surface;it’s the new operating layer.

- Private, continuous evaluation is mission-critical:Public benchmarks aren’t enough.Enterprises demand trusted, explainable performance.Build in eval infrastructure from day one.

- Speed of implementation is a strategic advantage:Onboarding that once took months now takes hours.Codegen, auto-mapping, and natural language interfaces collapse vendor lock-in.

- Vertical AI is the new SaaS:"Technophobic" industries are adopting AI fast.Win by embedding deeply, proving ROI from day one, and scaling quickly.

- Incumbents are awake—and acquisitive:SaaS giants are buying their way into AI.Build technical and data moats.Be M&A-ready, but operate like you’ll own the category.

- Taste and judgment are your differentiators:In a world of agents and automation, human insight is the edge.Founders who intuit what should exist—not just what can—will define the next era.

The founder’s edge is shifting.Speed alone isn’t enough.You need product intuition, empathy, and clarity of purpose.You don’t just need a better model—you need a better model of the world.The companies that win next won’t do more AI.They’ll do the right AI—at the right altitude, with the right outcome.

The AI universe is expanding fast.Now is the time to build the gravity that holds your galaxy together.Let’s go.